Originally posted by Michael Grogan.

The below is an example of how sklearn in Python can be used to develop a k-means clustering algorithm.

The purpose of k-means clustering is to be able to partition observations in a dataset into a specific number of clusters in order to aid in analysis of the data. From this perspective, it has particular value from a data visualisation perspective.

This post explains how to:

- Import kmeans and PCA through the sklearn library

- Devise an elbow curve to select the optimal number of clusters (k)

- Generate and visualise a k-means clustering algorithms

The particular example used here is that of stock returns. Specifically, the k-means scatter plot will illustrate the clustering of specific stock returns according to their dividend yield.

1. Firstly, we import the pandas, pylab and sklearn libraries. Pandas is for the purpose of importing the dataset in csv format, pylab is the graphing library used in this example, and sklearn is used to devise the clustering algorithm.

import pandas

import pylab as pl

from sklearn.cluster import KMeans

from sklearn.decomposition import PCA

2. Then, the ‘sample_stocks.csv’ dataset is imported, with our Y variable defined as ‘returns’ and X variable defined as ‘dividendyield’.

variables = pandas.read_csv('sample_stocks.csv')

Y = variables[['returns']]

X = variables[['dividendyield']]

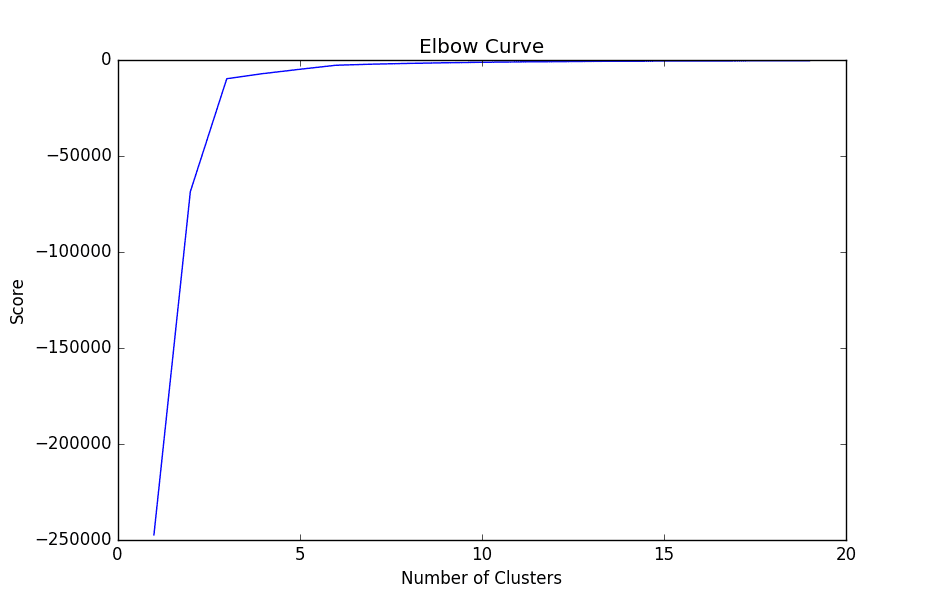

3. The elbow curve is then graphed using the pylab library. Specifically, we are devising a range from 1 to 20 (which represents our number of clusters), and our score variable denotes the percentage of variance explained by the number of clusters.

Nc = range(1, 20)

kmeans = [KMeans(n_clusters=i) for i in Nc]

kmeans

score = [kmeans[i].fit(Y).score(Y) for i in range(len(kmeans))]

score

pl.plot(Nc,score)

pl.xlabel('Number of Clusters')

pl.ylabel('Score')

pl.title('Elbow Curve')

pl.show()

When we graph the plot, we see that the graph levels off rapidly after 3 clusters, implying that addition of more clusters do not explain much more of the variance in our relevant variable; in this case stock returns.

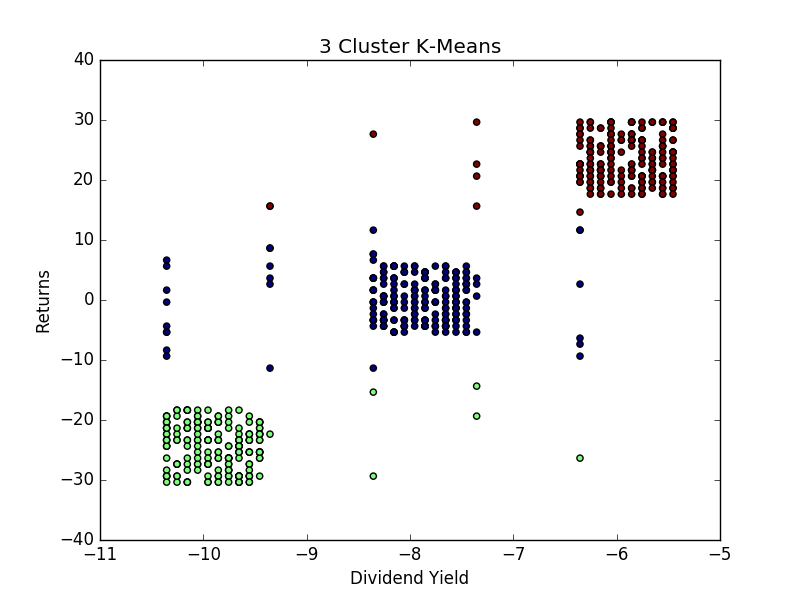

4. Once the appropriate number of clusters have been identified (k=3), then the pca (Principal Component Analysis) and kmeans algorithms can be devised.

The purpose behind these two algorithms are two-fold. Firstly, the pca algorithm is being used to convert data that might be overly dispersed into a set of linear combinations that can more easily be interpreted.

pca = PCA(n_components=1).fit(Y)

pca_d = pca.transform(Y)

pca_c = pca.transform(X)

From Step 3, we already know that the optimal number of clusters according to the elbow curve has been identified as 3. Therefore, we set n_clusters equal to 3, and upon generating the k-means output use the data originally transformed using pca in order to plot the clusters:

kmeans=KMeans(n_clusters=3)

kmeansoutput=kmeans.fit(Y)

kmeansoutput

pl.figure('3 Cluster K-Means')

pl.scatter(pca_c[:, 0], pca_d[:, 0], c=kmeansoutput.labels_)

pl.xlabel('Dividend Yield')

pl.ylabel('Returns')

pl.title('3 Cluster K-Means')

pl.show()

From the above, we see that the clustering algorithm demonstrates an overall positive correlation between stock returns and dividend yields, implying that stocks paying higher dividend yields can be expected to have higher overall returns. While this is a more simplistic example and could be modelled through linear regression analysis, there are many instances where relationships between data will not be linear and k-means can serve as a valuable tool in understanding the data through clustering methods.

Originally posted here.

{kind=link}